How Do NEMT Brokers Get Paid?

NEMT brokers are intermediaries between NEMT payers and transportation providers that actually move patients. How a broker gets paid determines how they behave: their payment model dictates authorization decisions, reimbursement rates, and utilization pressure across the entire provider network. This article provides an insight into the broker’s financials, covers the two primary NEMT broker payment models, what drives rate levels, and reveals the payment challenges brokers commonly face, which can cause instability in the entire medical transportation ecosystem.

Contents:

- What Is an NEMT Broker Actually Being Paid For?

- The Two Main NEMT Payment Models

- How Model Choice and Contract Structure Work in Practice

- How broker compensation works in practice

- Conclusion

What Is an NEMT Broker Actually Being Paid For?

Non-emergency medical transportation brokers don't drive. They coordinate.

A payer, whether that's a state Medicaid agency, a Medicare Advantage plan, a VA regional office, or a self-insured employer, contracts with a broker to manage transportation benefits for the population they serve. The broker takes calls, vets and credentials transportation providers, assigns trips, tracks performance, and handles complaints. They do not set the rules; they are there to arrange the processes, distribute payments, and enforce the will of the payer upon the provider network.

According to the CCAM-TAC state-by-state profiles, over 40 states have chosen to administer their NEMT services through the broker model. Some Medicare Advantage plans also offer supplemental transportation benefits, and they have increasingly turned to the same broker networks. The VA's non-emergency transportation program runs through a separate federal contracting structure but draws on many of the same regional providers.

The Two Main NEMT Payment Models

The MACPAC Report to Congress identifies two primary payment mechanisms for Medicaid NEMT brokers: capitation and fee-for-service. Both appear across other payer types as well. They work in opposite directions financially, which is why understanding them matters. The payment model a broker operates under shapes nearly every decision they make about trips, providers, and cost control.

Capitation (per member per month)

Under capitation, brokers are paid a monthly “capitated” rate based on the number of eligible Medicaid members residing in their contracted region. This means that the broker gets a fixed monthly amount regardless of how many trips those members actually take. Here is an example: if 50,000 members live in a broker's territory and the capitation rate is $7 per member per month, the broker receives $350,000. So whether these members take 5,000 or 20,000 trips, the broker won’t get paid extra.

Within this model, the broker shoulders the financial risk. If members use more transportation than projected, the broker absorbs the loss, because the rides for passengers must be arranged, whether the broker turns a profit or not.

MACPAC data shows Medicaid capitation rates typically range from $4 to $10 per member per month, depending on benefit design and population health. Medicare Advantage rates are negotiated directly between brokers and plans and are not publicly reported, but the same per-member-per-month structure applies.

Advantages of the capitation (PMPM) payment model: Known and predictable revenue for the broker, while the payer gets rigid cost controls.

Major downside: The financial pressure on brokers can be immense. For instance, before the largest NEMT broker ModivCare filed for Chapter 11 bankruptcy in August 2025, they generated roughly 79% of revenue from capitated contracts. After years of margin compression, ModivCare's cost of services consumed roughly 85% of total revenue by 2024, illustrating just how thin capitation economics can get.

Moreover, the PMPM risk structure has a direct effect on trip authorization. A capitated broker has a financial incentive to limit trip volume. This can lead to aggressive prior authorization, strict criteria for what qualifies as a covered trip, or causes delays in credentialing new providers. If the capitation model is not applied correctly, it can become yet another barrier to healthcare access.

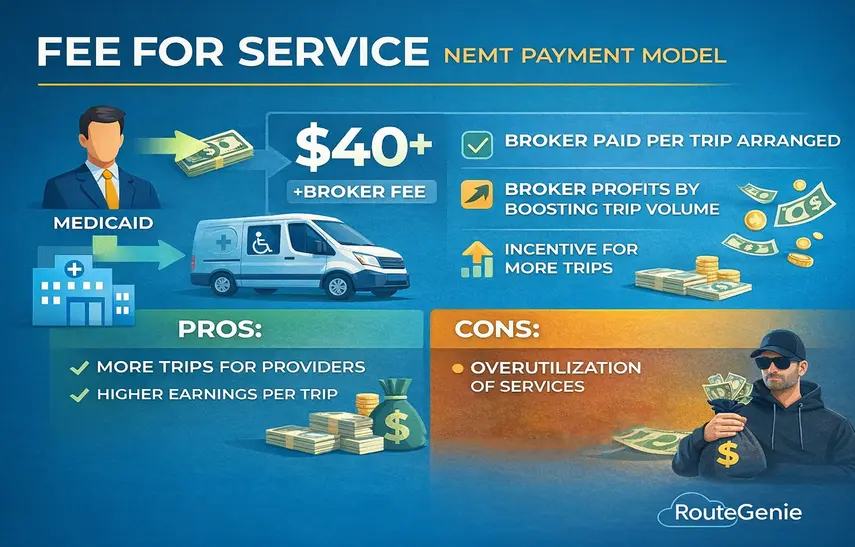

Fee-for-service NEMT payment model

Under fee-for-service, the payer pays the broker separately for each trip arranged. The rate is typically a base trip cost plus an administrative fee. The broker earns more by arranging more trips.

Advantages of the fee-for-service payment model: brokers and providers potentially can expect higher earnings per service, while passengers are likely to have better healthcare access.

Major downside: The incentive structure of the FFS model runs in the opposite direction from capitation. Instead of limiting utilization, FFS can potentially create financial motivation to increase it. This is well-documented in Medicaid NEMT data. New York state experienced taxi use, increase 800% and statewide NEMT spending rise 131% under a broker system with FFS-like billing. The GAO’s (U.S. Government Accountability Office) report on NEMT fraud documented roughly 200 criminal convictions, civil settlements, and judgments across 25 states from FY2015 to FY2020, with the most common fraud patterns being phantom rides and mileage inflation. The fraud patterns documented (phantom rides and mileage inflation) are a predictable result of billing structures that pay more for more trips.

Do NEMT brokers handle private pay?

Mostly no, but the answer depends on which type of broker you're dealing with.

Traditional brokers like MTM are built around government contracts, so a one-off private ride from a random individual doesn't fit that infrastructure. These companies function more as third-party administrators (TPAs) for health plans than as dispatch services for the general public.

That said, private pay does occasionally flow through brokers, but only in a specific scenario. Tech-first broker platforms might have consumer-facing portals that accept private bookings and route trips to their provider network, earning a margin on each one.

How Model Choice and Contract Structure Work in Practice

There isn’t a federally mandated broker payment model for NEMT. States are free to choose, and their decisions vary:

- States that prioritize budget predictability favor capitation. A fixed PMPM shifts utilization risk to the broker and makes annual spending easier to forecast. However, this choice forces MCOs to work only with larger national operators, who have sufficient financial reserves.

- FFS tends to appear in states with smaller programs, rural geographies where trip patterns are harder to model, or where the state wants direct visibility into individual trip costs. This may lead to overutilization, but if the NEMT program is run within a highly digitized environment using NEMT software for compliance, the fraud problem can be minimized.

In practice, both models operate inside formal contracts, and most contracts don't run purely one way or the other. An MCO payer might pay a broker on a capitated basis but embed FFS-style trip reporting requirements, performance withholds, and rate adjustments tied to utilization data. The contract is the major determinant of the payment framework. Capitation and FFS describe the dominant billing structure, but what a broker actually earns depends on how those structures are written, what performance triggers are attached, and which payer is on the other side of the table.

How broker compensation works in practice

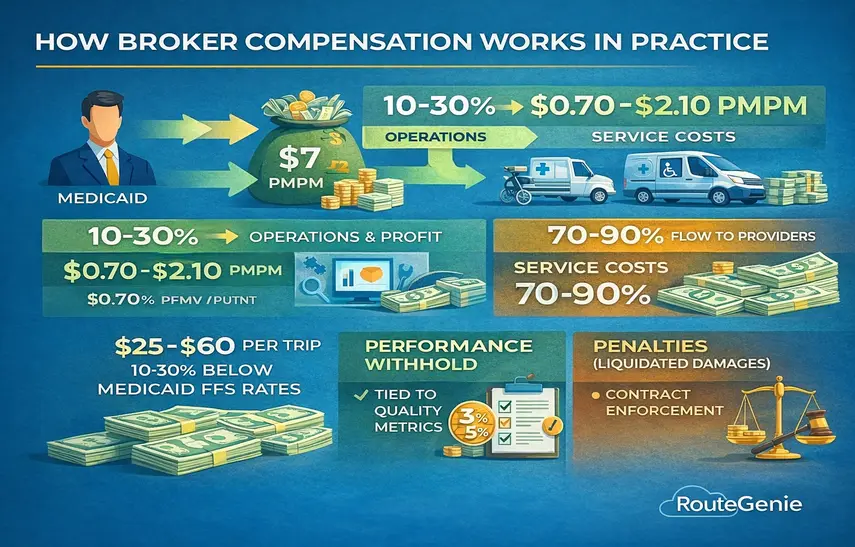

Brokers retain roughly 10 to 30% of capitation payments for operations, technology, and profit. The rest flows to providers. ModivCare's public filings showed approximately 88% of NEMT segment revenue paid out as service costs, meaning a $7 PMPM rate leaves the broker somewhere between $0.70 and $2.10 to run the entire coordination layer.

Provider per-trip rates typically land between $25 and $60 for standard ambulatory trips, often 10 to 30% below what states pay on direct Medicaid FFS.

Performance structures and financial accountability

Most contracts layer financial accountability on top of the base rate. Performance withhold (typically 3 to 5% of contract value) is released only when quality metrics are met. For example, Connecticut's Medicaid contract ties up to 5% of contract value to on-time rates, call center performance, and complaint volumes.

Both sides attempt to establish a synergetic relationship to ensure medical transportation continuity and reliability. Here are a couple of real-life examples. Risk corridors for the capitation model mean that states like Nevada cover 50% of the broker’s losses beyond 5%; in return, the broker's profit is limited to 2%. Liquidated damages are standard: Virginia's contract penalizes unfulfilled trips at 1% of the monthly payment per unmet standard; across all performance categories combined, LogistiCare paid nearly $2.5 million in fines between 2012 and 2015. The April 2025 HMA contracting report found some brokers now price anticipated penalties into their bids from the start.

What drives broker rates

Lastly, let’s address the $4 to $10 PMPM range for Medicaid capitation. Why is it that some brokers are making twice as few dollars as the others? The range is so wide because several factors push rates up or down.

Geography. Urban markets carry higher labor costs. Rural markets mean more deadhead miles per trip. Both cost more, and brokers negotiate rates accordingly.

Service complexity. A population with high wheelchair and stretcher volume costs more to serve than one that's mostly ambulatory. Payers build that into actuarial rate models.

Volume. Large brokers spread fixed costs. The economies of scale allow technology, call centers, compliance staff, and other expenses to be spread across more trips, giving them a cost advantage. Smaller regional brokers can still compete where they know the provider landscape well.

Competition. Virginia's Joint Legislative Audit and Review Commission noted the state received only two viable bids in one recent NEMT procurement. Limited competition gives brokers more pricing power than a market with five or six serious bidders.

Track record. Brokers with clean audit histories and strong renewal records can hold firmer on rates because switching costs for payers are real. Replacing a broker mid-contract is operationally disruptive.

Conclusion

Whether your broker runs capitation or FFS shapes more than just how they get paid. It shapes what their financial incentives are, how hard they push on authorization, and ultimately how much of the payer dollar reaches your drivers. Understanding the model behind each nemt contract tells you what to expect and how to push back when something doesn't add up.

RouteGenie's broker integrations give operators a single interface for trip management, billing, and performance tracking across major brokers and payer types. If you're navigating multiple broker portals today, that's a high operational cost worth addressing.

About the author

As RouteGenie's Marketing Director, Yurii gained deep knowledge in the NEMT industry. He is an expert in marketing, leveraging all channels to build RouteGenie's brand and ensure NEMT providers have access to powerful NEMT software that can boost their growth. Yurii shares his knowledge by writing content on marketing and healthcare topics, including medical transportation, home care, and medical billing.