NEMT Industry Trends: What's Changing in 2026 and Beyond

The long-term growth trend in medical transportation remains positive. The growing number of beneficiaries and payers tying transportation to health outcomes is positive for NEMT providers. However, recent headlines paint a more cautious picture: shrinking benefits, fraud crackdowns, tightening compliance standards, and renewed fuel cost pressure. These are real pressures that can disrupt any operation, but it is reasonable to expect that these pressures will affect poorly organized operators the most, while disciplined providers will be able to consolidate and succeed. What follows is a look at the latest trends in non-emergency medical transportation in 2026 and beyond, where things stand, and how you can use these turbulent times as an opportunity to grow your business.

Contents:

- Population Trends and Demand: Market Size Projections

- Reimbursement Is Rising, but Providers Still Expect Higher Rates

- Fuel Costs Are Back in the Spotlight

- Workforce and Technology

- Brokers' Consolidation and Competition from Ridesharing

- Revenue Diversification and Value-based Care

- Compliance Pressure and Fraud Investigations

- NEMT provider playbook for 2026 and beyond

Population Trends and Demand: Market Size Projections

Demand for medical transportation is growing

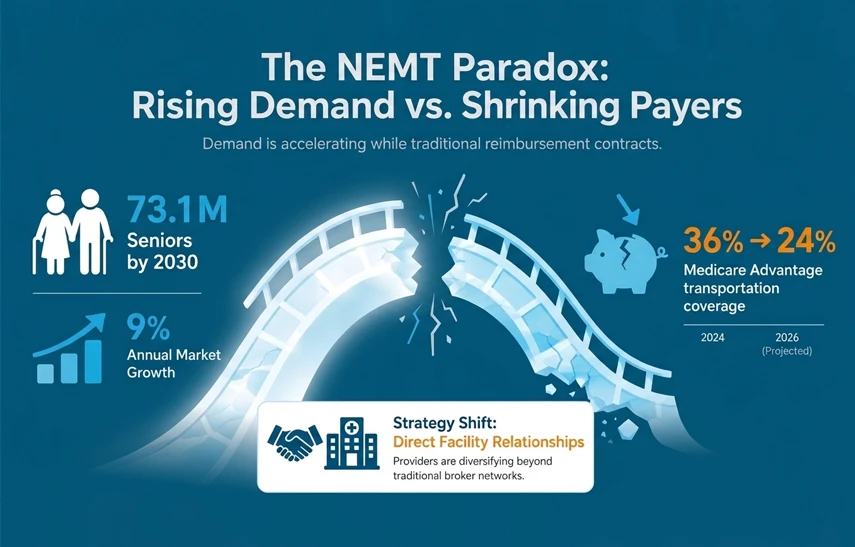

The patient population driving NEMT is getting larger. Older adults book three times more medical visits than younger people, and the U.S. Census Bureau projects 73.1 million Americans aged 65 and older by 2030 (up from 55.8 million today). Moreover, chronic conditions are on the rise, along with mental health and substance-use conditions. These people disproportionately require medical transportation, making the demand even more predictable. For instance, dialysis only supplies a solid volume: roughly 555,000 Americans are on dialysis, each requiring three round trips per week. With an estimated compound annual growth rate of 9% between 2026 and 2032, NEMT will not have a shortage of users.

Shifting payer landscape

However, where operators need to pay attention is the payer side. Medicaid contracts will be much stricter. Proposed Medicaid funding changes could remove 10 percent of people from eligibility over the next decade. Plus, KFF data shows Medicare Advantage plans offering transportation benefits are also declining. They dropped from 36% to 24% between 2024 and 2026.

So what are we seeing? The riders are there, but the payers' mix has to change. For operators already running a diversified operation, this is manageable. For those still dependent almost entirely on Medicaid broker volume, it's a reason to start building direct facility relationships before the trip volume moves.

Reimbursement Is Rising, but Providers Still Expect Higher Rates

The rate picture is more encouraging than it was two years ago, but transportation providers are still not out of the woods. Twenty-one states raised NEMT reimbursement in FY2024, including Illinois with a 40% average increase and Ohio at 79% for certain services, and fifteen more had increases planned for FY2025 to 2026.

The challenge is that despite these increases, broker rates haven't caught up with costs yet. The NEMTAC 2026 Rate and Cost Survey found 65 to 70% of providers calling current rates barely sustainable, and about 60% expect rural provider exit if nothing changes. Times are tough, but those providers who weather this storm will participate in the market with less competition for contracts and more negotiating leverage.

Fuel Costs Are Back in the Spotlight

Fuel is always a variable, but the 2026 picture is worth a closer look. The national average gas price hit $4.50 per gallon on May 12, up 43.6% year-over-year, with every state posting double-digit increases. California cleared $6.15, six states topped $5, and April 2026 became the sixth-highest month for gas prices on record. Middle East supply disruption is the driver, and EIA expects elevated prices through at least Q3.

For NEMT providers, the timing compounds an already tight rate picture. Providers were calling rates barely sustainable, and that was at $3.14 gas. Wheelchair vans get 12 to 16 mpg, so the per-trip fuel cost on a typical 15-mile round trip has climbed from roughly $3 to over $4 in twelve months.

Unlike trucking, where weekly EIA-indexed fuel surcharges are standard, NEMT broker contracts rarely include automatic fuel escalation. Providers carrying the cost have a few practical levers: negotiate fuel-escalation language into new broker SLAs, build fuel surcharges into private-pay and facility Master Service Agreements, audit routing efficiency to cut deadhead miles, and consider EVs on urban ambulatory routes under 20 miles. Fleets that move on these now reset their cost base before the next contract cycle.

Workforce and Technology

Medical transportation workforce

BLS projects 9% increase in employment demand in the driver category through 2034. Medical transportation will be responsible for a large portion of these job openings, since the aging population will require more professionals to transport them. However, the same demographic patterns that create transportation demand will cause workforce shortages. There aren’t enough young people entering the NEMT labor force, and those who do are expected to have an annual turnover of over 64%. Because replacing each driver is a costly matter, the new focus for companies should not be recruitment, but employee retention.

Technology is the most direct tool for that. Dispatch and scheduling platforms with AI capabilities reduce deadhead miles, cut the administrative burden on drivers, and lower claim denial rates. Lighter admin load and more predictable schedules are two of the most common reasons drivers cite for leaving, and software addresses both without requiring large wage increases. That's where the near-term technology investment pays off most clearly.

Autonomous medical transport

Autonomous vehicles will eventually reach medical transportation, but the timeline and the way they will be utilized matter more than the headline. There are pilot programs with ambulatory and even wheelchair-accessible autonomous vehicles in Detroit and California, explicitly serving medical facility patients. However, the state of autonomy technology and legislation suggests that, for now, core NEMT services will stay with compliant NEMT providers. Door-through-door service and mobility device securement aren't problems AVs solve today, which means high-acuity operators have years to build positions before automation touches their segment.

Electric vehicles in NEMT

With the rising fuel prices, EVs are worth looking at now for urban ambulatory routes specifically. Running costs average $0.59/mile versus $0.85 to $0.98 for gasoline, a saving of roughly $6,000 to $9,000 per vehicle per year, and some parts of the nation offer programs that cover a large portion of purchase costs. Wheelchair-accessible EV options remain limited, but there are already at least 7 electric NEMT vans that can do the job. For now, ambulatory routes under 20 miles are the practical entry point.

Brokers' Consolidation and Competition from Ridesharing

The broker landscape changed significantly in 2024 and 2025. ModivCare filed Chapter 11 in August 2025, emerged 117 days later after cutting $1.1 billion in debt, and kept paying providers throughout. Around the same time, MTM acquired Access2Care, adding coverage across all 50 states. The verdict? The market is rapidly consolidating around larger brokers.

That's not necessarily bad for providers. Fewer, better-capitalized brokers tend to mean more stable payment timelines and clearer performance expectations. The operators who felt the most pressure during ModivCare's restructuring were those with no revenue outside broker contracts. Those with a large volume of direct facility relationships fared much better.

And what about competition coming from ridesharing giants? Lyft Healthcare and Uber Health are gaining ground in ambulatory transport, but neither can serve wheelchair, stretcher, or door-through-door patients. Wheelchair vans are 43% of the entire NEMT market, and every broker contract mandates ADA-compliant service. If you specialize in high-acuity transport, you're operating in a market that rideshare legally cannot enter. Therefore, during the spikes in demand, it makes sense to offload less lucrative ambulatory rides to rideshare and maximize utilization of specialized vans for wheelchair and stretcher contracts.

Revenue Diversification and Value-based Care

Rate pressure from brokers makes payer diversification less optional every year. The most reliable starting point is dialysis centers. Patients have 156 trips a year on a predictable schedule, and private-pay rates run $75 to $150 per trip compared to $40 to $60 under Medicaid. Dialysis and oncology patients, hospital discharge contracts, and specialized stretcher NEMT may represent a low percentage of trip volume, but bring in disproportionately higher pay.

Value-based medical transportation model

Beyond that, the industry is moving from volume to value-based medical transportation models, and that's starting to pay. CMS's In Lieu of Services framework lets MCOs spend up to 5% of every premium dollar on social determinants of health, transportation included, and count it toward their medical loss ratio. Connecticut already ties up to 5% of broker contract value to performance metrics as bonuses. Operators who document trip completion rates and appointment adherence can pitch themselves to health plans as a care partner rather than a logistics vendor. That's a fundamentally different conversation than competing on per-trip rate.

The April 2025 HMA contracting report found operators meeting performance thresholds are increasingly earning withholds back as bonuses, which means documented quality is becoming a revenue line.

Compliance Pressure and Fraud Investigations

HHS OIG announced targeted NEMT fraud reviews in October 2025, and several states have moved to enrollment moratoriums with unannounced site visits. For operators running clean operations, this is good news. Fraud inflates trip counts, distorts rate negotiations, and fills the market with providers who undercut pricing they can only sustain through billing manipulation. When they exit, they leave trips and contracts behind.

The compliance requirements that go alongside these reviews act as a barrier to entry that rewards providers already meeting the standard. GPS trip verification is now mandatory in Texas, Florida, California, New Jersey, and New York, and HIPAA enforcement is becoming more strict. These raise costs across the board, but operators already running compliant systems gain ground while others scramble to catch up.

Interestingly, there isn’t a federal NEMT standard, but organizations like NEMTAC provide accreditation that many recognize as the benchmark in medical transportation compliance.

NEMT provider playbook for 2026 and beyond

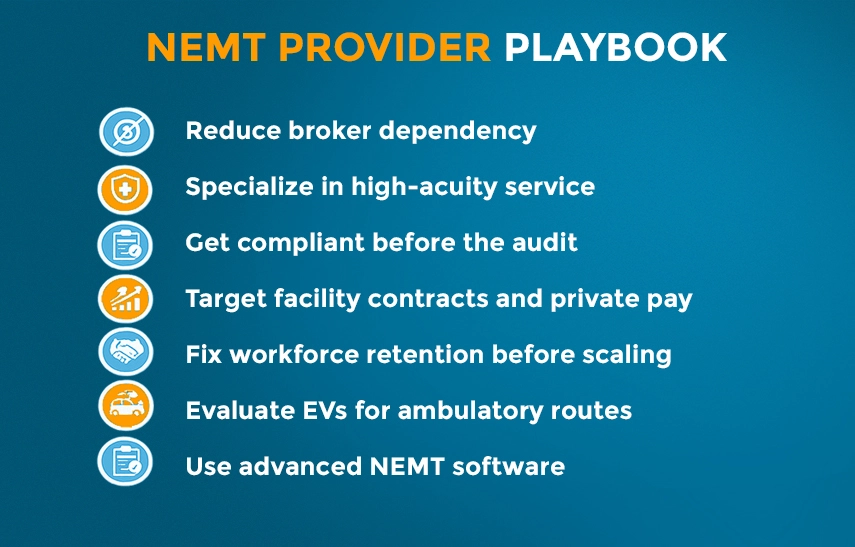

Every trend above points in the same direction: diversified, compliant, data-driven operators will be best positioned to succeed in the changing NEMT landscape. Here's what that looks like in practice.

- Reduce broker dependency: Direct contracts with dialysis centers, hospitals, and assisted living facilities hold their value regardless of what happens in the broker tier. Build toward a revenue stream equally split between brokers, facility contracts, and private pay customers.

- Specialize in high-acuity service: Wheelchair and stretcher transport pays 2 to 3x ambulatory rates, and unlike ambulatory sedans, they have no credible rideshare competition. Use rideshare strategically for overflow orders.

- Get compliant before the audit: GPS trip verification, HIPAA-compliant dispatch, and NEMTAC accreditation are becoming contract requirements in more states each cycle.

- Use advanced NEMT software: On-time performance, trip completion rates, and clean claims ratios are what open value-based and ILOS contracts. Without them, you're competing on price alone.

- Target facility and private pay contracts: Fight for hospital discharge contracts, dialysis and oncology centers, substance-use and mental health facilities.

- Fix workforce retention before scaling: Better scheduling and lighter admin load reduce driver churn without large wage increases. Retention is cheaper than recruitment at every fleet size.

- Maximize fleet efficiency: Cut deadhead miles with sophisticated routing software, audit route performance against actual fuel and labor costs, and pilot EVs on urban ambulatory routes under 20 miles. Fuel volatility makes routing efficiency a margin lever, not a nice-to-have.

73 million Americans will turn 65 by 2030. The operators who capture that demand are building for it now.

RouteGenie helps NEMT operators manage broker integrations, GPS trip verification, compliance reporting, and route optimization across multi-broker and multi-payer operations.

About the author

Serhii Taborovskyi is the founder and author of the Automotive Territory YouTube Channel, with 300,000 subscribers and counting. He is an avid automotive enthusiast and a fan of any and all motorized vehicles. Serhii is a visiting author at RouteGenie, sharing his expertise for the benefit of the NEMT community.